The Canadian Prefab Mortgage Checklist: What Lenders Look For in 2026

General

Admin

5/15/20265 min read

The Canadian Prefab Mortgage Checklist: What Lenders Look For in 2026

You have chosen a prefab or modular home for your next build. The design is finalized, the factory is ready, and you are excited to get started. But when you approach a Canadian lender for a mortgage, will they treat your factory-built home the same as a traditional house? The answer depends on three specific factors. Get them right, and you qualify for standard mortgage rates with as little as 5% down. Miss one, and you could be looking at chattel financing with significantly higher costs. This checklist walks you through exactly what Canadian lenders evaluate, from CSA certifications to foundation requirements and the new CMHC Prefab Plus program.

The Three-Factor Test: What Every Canadian Lender Checks

In Canada, lenders evaluate every prefab home mortgage application against three specific criteria. All three must be satisfied for conventional mortgage financing.

❏ Factor 1: CSA A277 Certification

The CSA A277 standard is a quality assurance and factory inspection protocol for modular construction. It confirms that your home was built under third-party inspection to comply with the National Building Code (NBC) and applicable provincial codes. Lenders treat CSA A277 certification as the baseline signal that the home was built to the same standard as a site-built property.

The critical distinction:

CSA A277 = modular home = treated like a regular house (full mortgage options)

CSA Z240 = manufactured/mobile home = treated like a specialty product (restricted options, higher rates)

What to do: Always request CSA A277 certification documentation from your builder before committing to any financing structure. This is the single most important piece of paperwork in your file.

❏ Factor 2: Permanent Foundation

Lenders require your home to be installed on a permanent foundation—a concrete basement, concrete crawlspace, or engineered footings designed for the specific site and soil conditions.

Why this matters: A permanent foundation converts the home from personal property (chattel) to real property, which is what a mortgage is secured against. A home placed on blocks, piers, or temporary supports will generally NOT qualify for conventional mortgage financing.

What to budget: Foundation costs vary significantly by region and site conditions. Rocky terrain, slope, and soil type all affect costs. Budget in the range of 20,000 to 60,000 or more, depending on your site.

❏ Factor 3: Fee Simple Title (Owned Land, Not Leased)

The home and land must be registered as a single real property on the land title. This happens automatically when a CSA A277-certified modular home is permanently installed on a lot the buyer owns in fee simple.

The critical distinction:

Fee simple ownership (you own the land) = conventional mortgage, 5% down minimum, full lender pool

Leased land (mobile home park, rented lot) = chattel financing, 20-35% down, higher rates, limited lenders

What to do: Ensure you either own the land outright or have a purchase agreement for it before applying for a mortgage. Most mortgage products require owned land, not leased.

CMHC Mortgage Insurance: The 5% Down Path

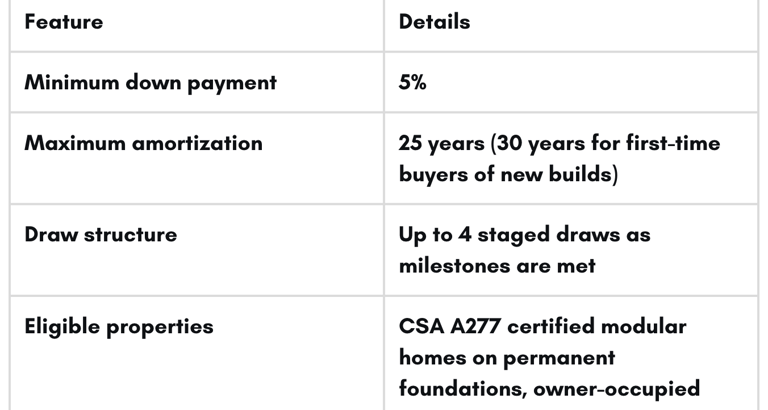

New for 2026: CMHC has launched CMHC Prefab Plus, a new mortgage loan insurance product specifically designed for prefabricated and modular homes. This is a game-changer for Canadian prefab buyers.

CMHC Prefab Plus Features

The staged draw structure is designed to match how prefab homes are actually built and delivered: one draw to acquire and prepare the site, a subsequent draw once the home is delivered and ready for installation, and final draws upon completion.

CMHC Eligibility Criteria

To qualify for CMHC-insured financing (including Prefab Plus), your home must meet all four of these criteria simultaneously:

Permanently affixed to a permanent foundation

CSA A277 factory certified

Compliant with the applicable provincial building code

Used as your owner-occupied primary residence on owned land (not leased land, not seasonal/recreational)

When all four conditions are met, CMHC insurance allows eligible buyers to purchase with as little as 5% down—the same minimum down payment that applies to conventional site-built home purchases.

Alternative insurers: Canada Guaranty and Sagen (formerly Genworth) are alternative providers of default mortgage insurance in Canada and apply similar eligibility criteria for factory-built homes on owned land with CSA certification.

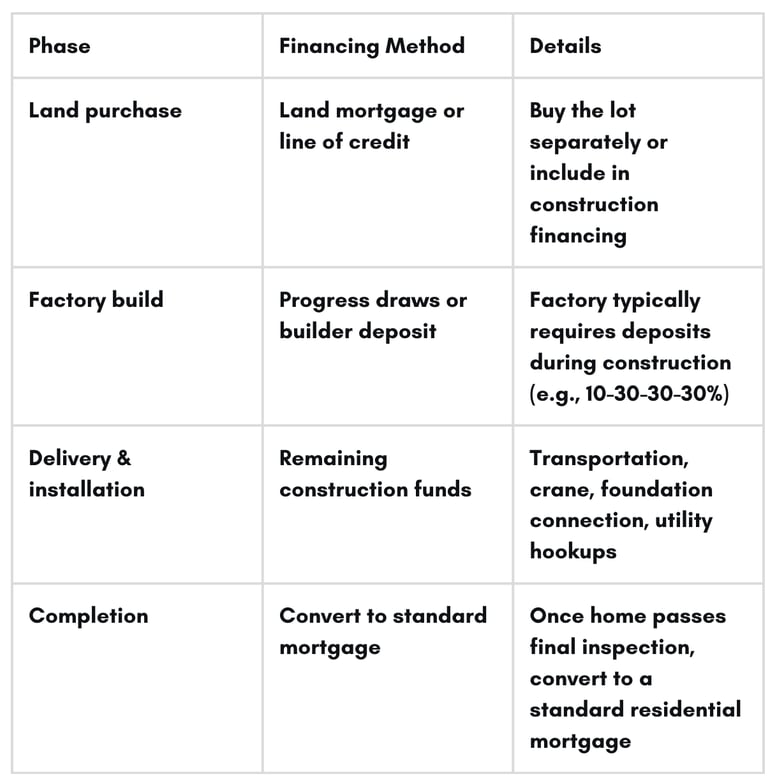

The Financing Timeline: How It Works

Because modular homes are built in a factory before delivery, the financing timeline differs from site-built construction:

The challenge: The gap between when the factory needs payment and when the mortgage funds are released. You may need bridge financing or a construction loan because the mortgage is not finalized until the home is complete and inspected on its foundation.

The solution: CMHC Prefab Plus is designed specifically to address this by allowing staged draws that align with actual construction milestones.

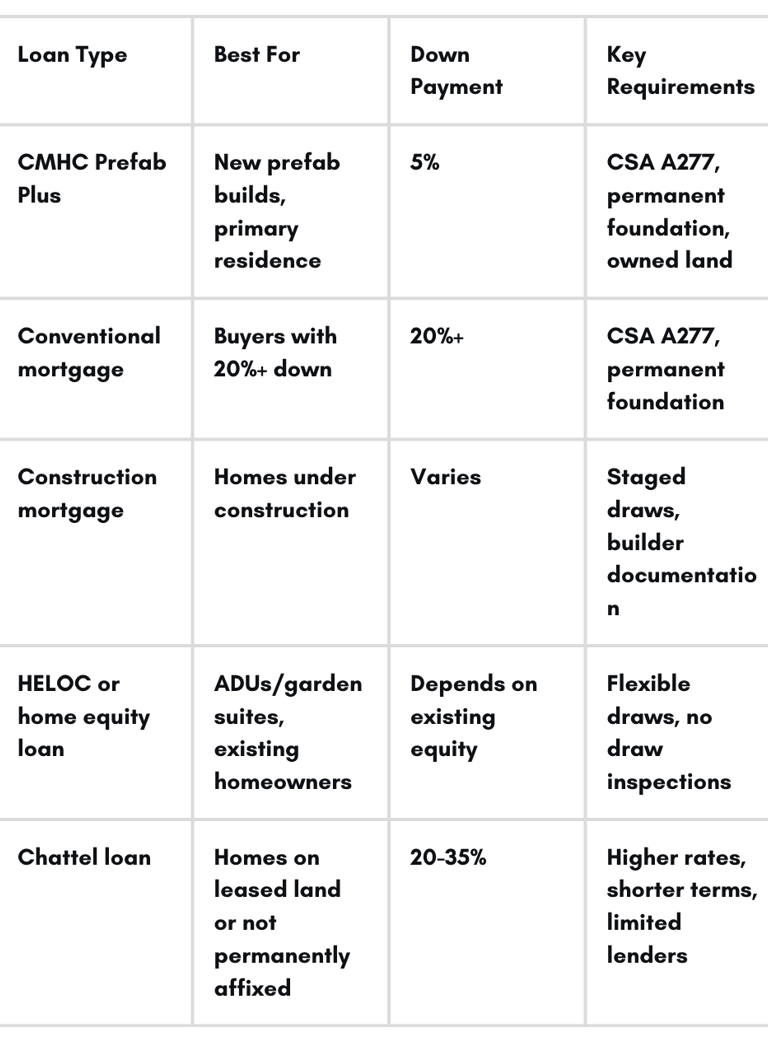

Loan Types Available for Canadian Prefab Homes

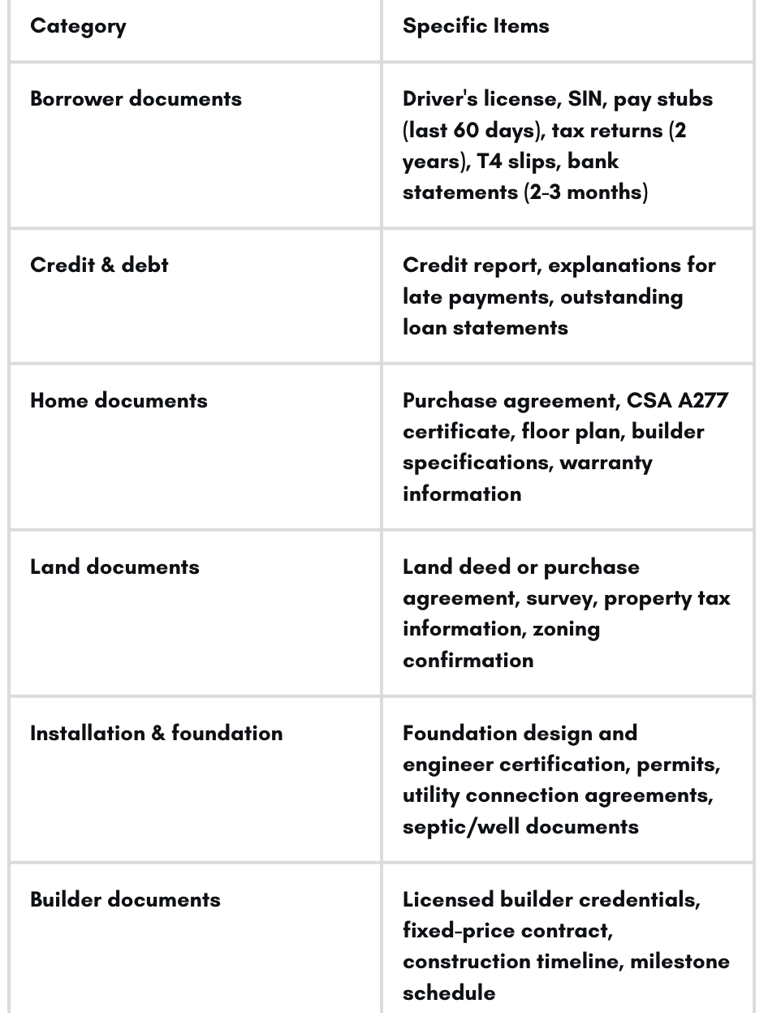

Required Documentation: What to Gather Before Applying

Lenders will ask for the same documentation they need for any home loan, plus prefab-specific items :

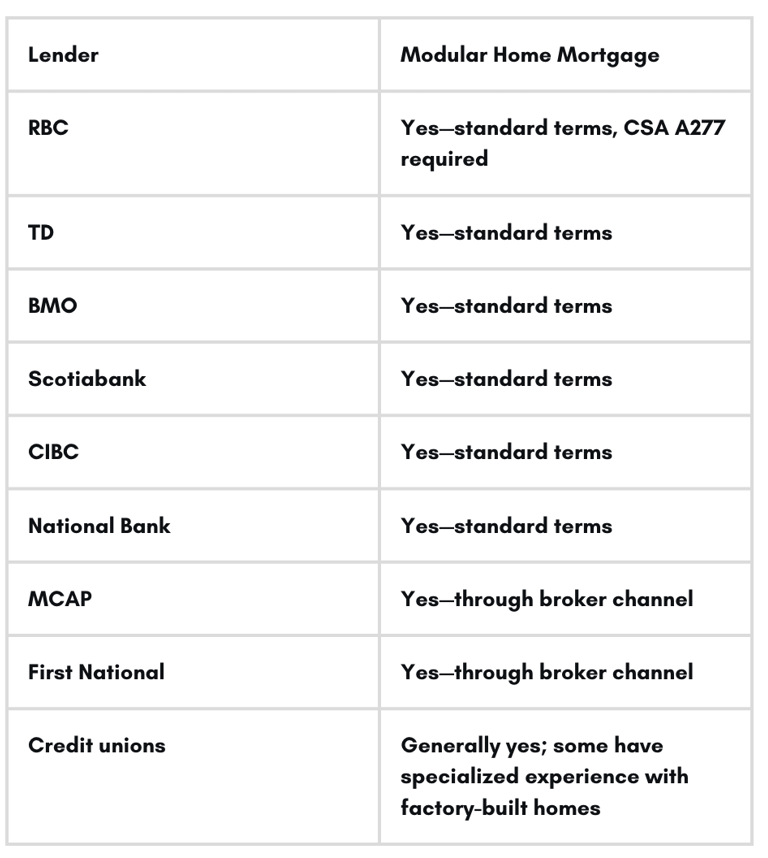

Canadian Lenders Who Finance Modular Homes

All major Canadian banks and many credit unions offer standard mortgage terms for CSA A277-certified modular homes on permanent foundations and owned land :

How PrefabIQ Helps Canadian Buyers Get Mortgage-Ready

Navigating Canadian lender requirements—especially the CSA A277 certification and CMHC Prefab Plus draw schedule—requires careful documentation. PrefabIQ simplifies the process:

Compliance Management: Track CSA A277 certification status, builder credentials, and permit requirements in one dashboard

Documentation Hub: Store land deed, builder contract, engineering drawings, and inspection reports with secure, shareable access

Milestone Tracking: Align construction draws with CMHC Prefab Plus requirements—automated reminders when draws are due

Stakeholder Hub: Give your lender, builder, and lawyer secure access to real-time project updates, reducing back-and-forth delays

When your lender can see the complete picture—certification, foundation plan, permits, and timeline—approval happens faster, and draws are released on schedule.

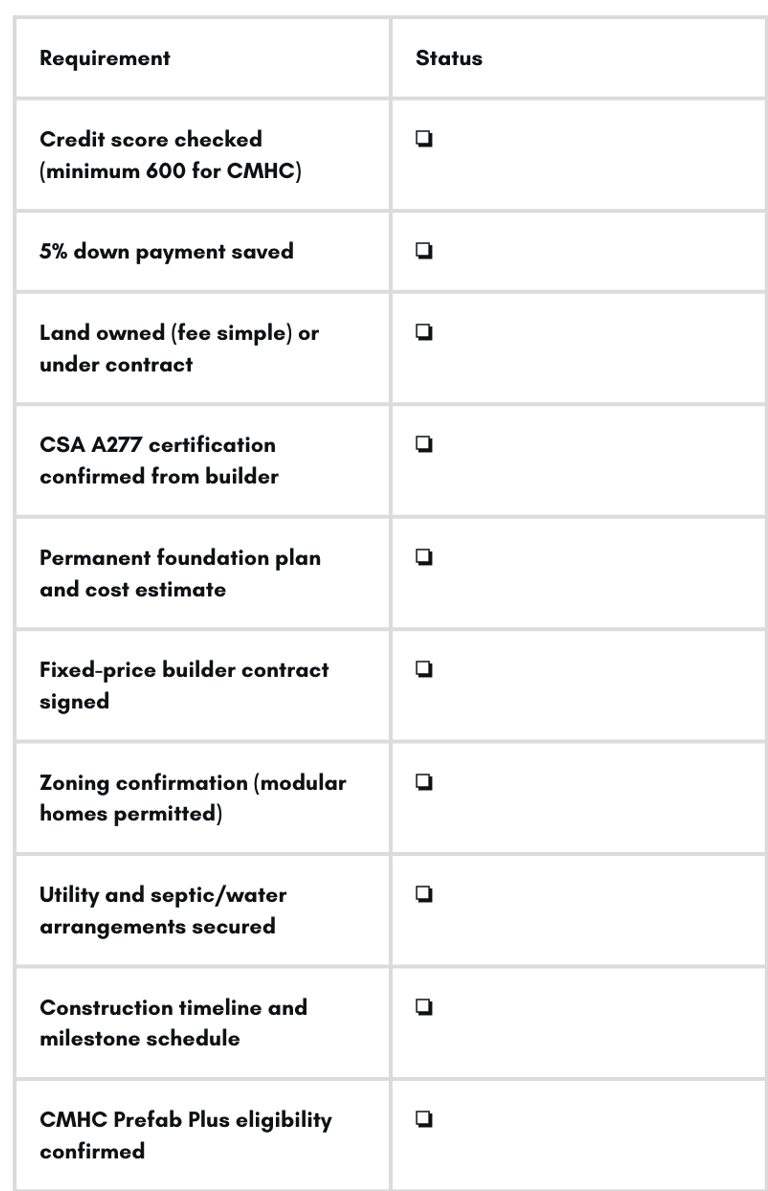

Final Checklist: Before You Talk to a Canadian Lender

Use this checklist to ensure you are fully prepared:

The bottom line: Prefab and modular homes are fully financeable in Canada—often on identical terms to site-built homes. The three-factor test (CSA A277, permanent foundation, fee simple title) determines your path. Get these right, and you are looking at standard mortgage rates with as little as 5% down. Miss one, and you face higher costs and fewer options. With proper preparation and the right documentation, your factory-built Canadian home is within reach.

PREFAB SOLUTIONS

LOCATION

STAY UPDATED

info@prefabsolutions.ca

© 2025. ALL RIGHTS RESERVED

1000784075 ONTARIO CORPORATION OCN/BIN Numéro de société de l’Ontario/NIE: 1000784075

CONTACT

We are a digital first company based in Toronto, Ontario, Canada

SOCIAL

OUR BRANDS

Prefab Essentials

Prefab Match

Prefab Collective

The Modularity Group Inc. is a company with multiple business holdings. Prefab Solutions serves consumers with prefab construction advocacy. PrefabIQ serves consumers with housing construction and management software. Prefab Match is in the housing listing industry. Prefab Essentials retails premium décor and furnishings. , while Prefab Collection offers a membership-based community for enthusiasts to share and learn. While each company operates as a separate entity, we all function on the foundational principle: the future of living is also modular, it is smarter, it is more flexible, it is about precision over excess, and community over going it alone. We believe a well-designed home is a symphony of integrated parts—a harmonious blend of space, light, and function.

D-U-N-S NUMBER 243369819