The Prefab Home Mortgage Checklist: What US Lenders Look For in 2026

General

Admin

5/12/20265 min read

The Prefab Home Mortgage Checklist: What US Lenders Look For in 2026

You've found the perfect prefab or modular home. The design is locked in, the land is ready, and you're excited to break ground. But when you walk into a bank to apply for a mortgage, will they treat your factory-built home the same as a traditional house? The short answer is yes—provided you meet specific requirements. Understanding what lenders look for before you apply can mean the difference between a smooth approval and weeks of frustrating delays. This checklist walks you through exactly what US lenders evaluate when financing a prefab or modular home, from credit requirements to foundation standards and everything in between.

The Good News: Modular Homes Are Treated Like Site-Built Homes

Once your modular home is installed on a permanent foundation, banks classify it as real property—the same as any stick-built house. This means you qualify for the same loan types, interest rates, and terms as conventional home buyers .

The key distinction is between:

Lenders actually prefer modular homes because they appreciate in value like regular houses. The construction quality often exceeds site-built homes thanks to factory precision and weather-protected building conditions .

The Prefab Mortgage Checklist: 7 Requirements Lenders Verify

Before approving your loan, lenders will work through this checklist. Use it to prepare your application.

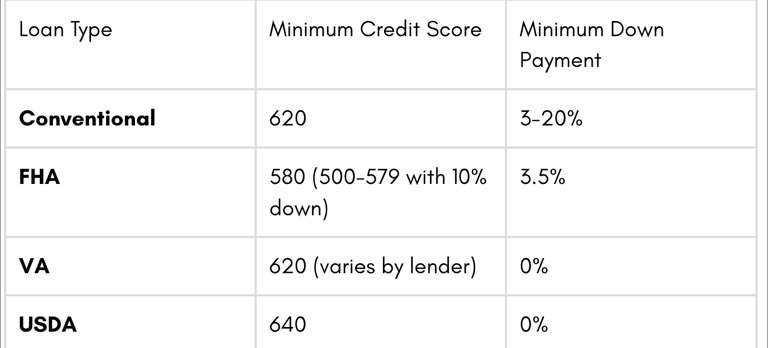

❏ 1. Credit Score & Financial Health

Your personal finances are the first thing lenders review. Requirements vary by loan type:

Lenders will also evaluate:

Debt-to-income (DTI) ratio: Most lenders want below 43%

Employment history: 2+ years of stable income

Payment history: No late payments in the past 12 months preferred

Pro tip: Get pre-approved before you choose a home model. This tells you exactly what you can afford and shows sellers you're serious.

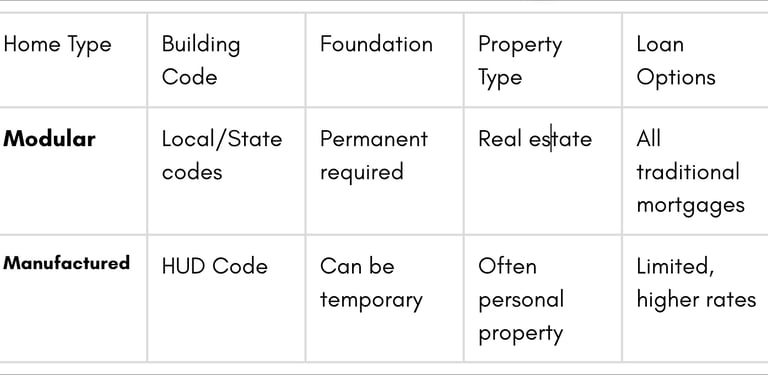

❏ 2. Property Classification: Modular vs. Manufactured

This is the single most important factor. Lenders draw a hard line between modular and manufactured homes:

Modular homes are built to the same local and state building codes as site-built homes. They qualify for all traditional mortgage products.

Manufactured homes are built to federal HUD Code standards. They may require specialized loans like FHA Title I or II, and often carry higher interest rates (8-11% vs. 6.5-7.5% for modular).

What to check: Ensure your home's documentation clearly identifies it as a modular home built to local codes, not a manufactured home built to HUD standards.

❏ 3. Permanent Foundation Requirement

For any traditional mortgage, your home must sit on a permanent foundation—a concrete basement, crawlspace, or slab designed and engineered for the specific site .

Why this matters: A permanent foundation converts the home from personal property (chattel) to real property, which is what a mortgage is secured against . Homes on blocks, piers, or temporary supports generally will NOT qualify for conventional financing.

What to budget: Foundation costs typically range from 20,000to20,000to60,000 or more depending on site conditions, soil type, and regional labour rates .

❏ 4. The HUD Label (For Manufactured Homes)

If you are financing a manufactured home (rather than modular), lenders will look for:

Red HUD certification labels attached to each transportable section

Data plate with manufacturer, serial number, wind zone, roof load, and thermal zone information

Minimum size: At least 400 square feet of floor area for FHA loans

Build date: After June 15, 1976 (when HUD Code took effect)

Without these labels and documentation, FHA and conventional financing may be impossible.

❏ 5. Land Ownership & Site Documentation

Lenders need to know exactly where your home will sit. You'll need to provide:

Land deed or purchase agreement

Site plan showing the building envelope and setbacks

Zoning confirmation that factory-built homes are permitted on the property

Utility agreements for water, sewer/septic, and power

If you are leasing land (e.g., in a mobile home park), most traditional mortgages will NOT be available. You would be looking at chattel financing instead—which carries higher rates and shorter terms .

❏ 6. Builder & Contract Documentation

Lenders will scrutinize your builder contract. Ensure it includes:

Fixed-price contract with itemized costs: home model, dimensions, finishes, delivery, setup, foundation, utility connections, and site work

Licensed builder registered in the state where the home will sit

Warranty information: 1-year full warranty is standard; look for 2-5-10 structural warranty

Construction timeline with milestone dates

A vague or incomplete contract is a major red flag for underwriters.

❏ 7. Appraisal & Comparable Sales

The lender will require an appraisal to confirm that the completed home will be worth at least the loan amount. For modular homes:

The appraiser will compare your home to site-built homes in the area—not other factory-built homes

The home must meet minimum property standards for safety, security, and soundness

For new construction, lenders require an "as-completed" appraisal before releasing final funds

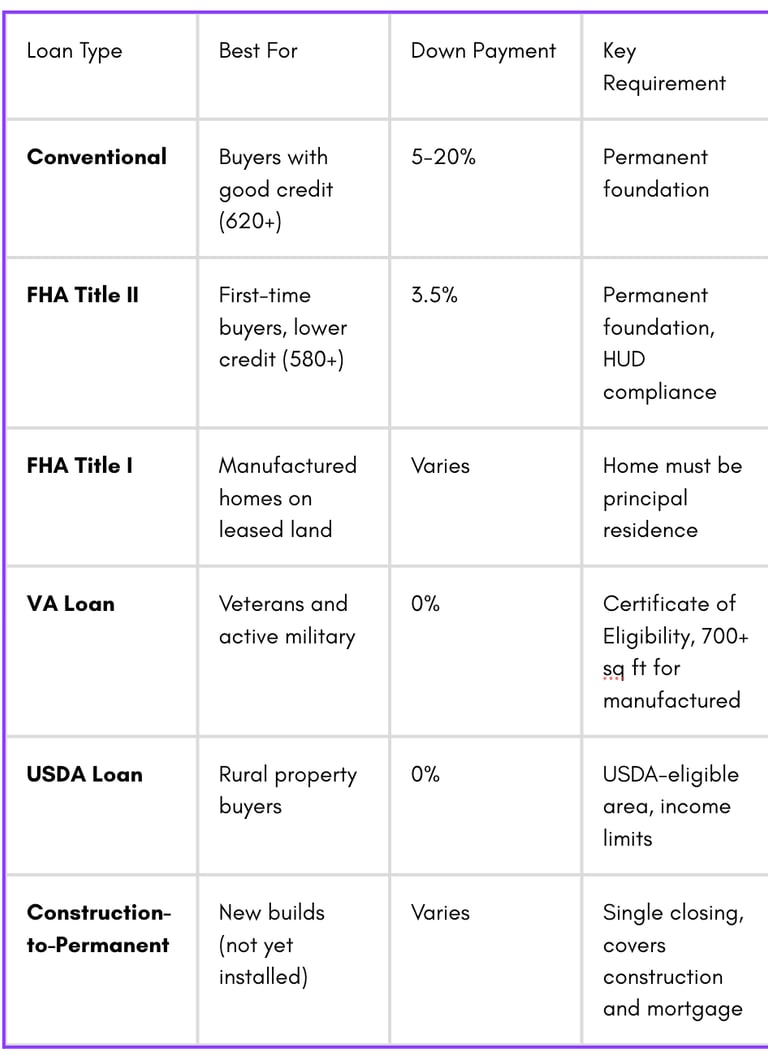

Loan Types Available for Prefab Homes

Depending on your situation, one of these loan types will likely be your best fit:

The Two-Stage Financing Process

If you are building a new prefab home (rather than buying one already installed), your financing will typically work in two stages :

Stage 1: Construction Loan

Short-term loan covering the manufacturing and installation period (typically 3-12 months)

Interest-only payments during construction

Funds released in "draws" as milestones are reached (factory completion, delivery, installation)

Stage 2: Permanent Mortgage

Converts automatically once construction finishes

Standard 15-30 year amortization

Principal and interest payments begin

Many lenders offer construction-to-permanent loans that bundle both stages into one package, saving you closing costs and simplifying paperwork .

How PrefabIQ Helps You Get Mortgage-Ready

Navigating lender documentation requirements is one of the biggest challenges in prefab financing. PrefabIQ simplifies this process by centralizing everything lenders need:

Documentation Hub: Store and organize your land deed, builder contract, permits, and engineering drawings in one secure location

Compliance Management: Track CSA A277 certification (for Canadian builds) or HUD compliance (for US builds) with automated reminders

Project Timeline: Share real-time construction progress with your lender to facilitate smooth draw requests

Stakeholder Hub: Give your lender, builder, and legal team secure access to the same up-to-date information

When your lender can see the complete picture—land ownership, builder credentials, permits, and project timeline—approval happens faster.

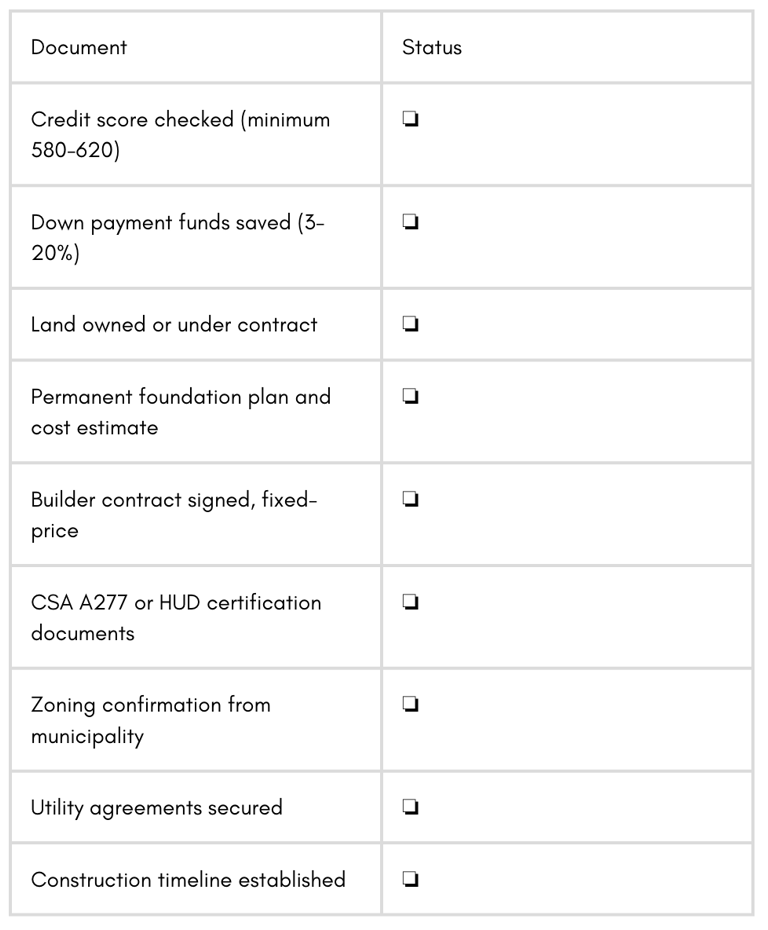

Final Checklist: Before You Apply

Use this checklist to ensure you're ready to walk into a lender's office:

The bottom line: Modular homes are financeable—often on identical terms to site-built homes. The key is understanding the requirements before you apply, choosing the right loan product, and having your documentation organized. With proper preparation, your factory-built dream home is within reach.

PREFAB SOLUTIONS

LOCATION

STAY UPDATED

info@prefabsolutions.ca

© 2025. ALL RIGHTS RESERVED

1000784075 ONTARIO CORPORATION OCN/BIN Numéro de société de l’Ontario/NIE: 1000784075

CONTACT

We are a digital first company based in Toronto, Ontario, Canada

SOCIAL

OUR BRANDS

Prefab Essentials

Prefab Match

Prefab Collective

The Modularity Group Inc. is a company with multiple business holdings. Prefab Solutions serves consumers with prefab construction advocacy. PrefabIQ serves consumers with housing construction and management software. Prefab Match is in the housing listing industry. Prefab Essentials retails premium décor and furnishings. , while Prefab Collection offers a membership-based community for enthusiasts to share and learn. While each company operates as a separate entity, we all function on the foundational principle: the future of living is also modular, it is smarter, it is more flexible, it is about precision over excess, and community over going it alone. We believe a well-designed home is a symphony of integrated parts—a harmonious blend of space, light, and function.

D-U-N-S NUMBER 243369819